COST SAVING SOURCES FROM SFA IN UNORGANIZED RETAIL SALES CONTEXT (URC)

In one of my previous blogs, I introduced cascading layers of characteristics a field automation solution must possess in unorganized retail based selling context-URC(e.g. via distribution network)and mentioned I would detail out on specifics of each layer for Unorganized retail context in separate blogs.

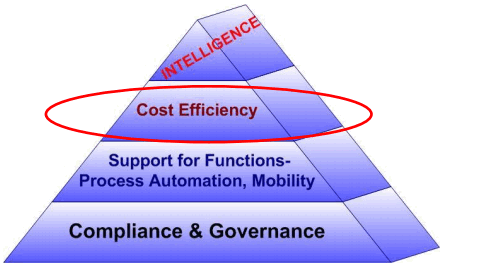

For sake of continuity, let me reproduce the cascading layers as below:

The focus of this blog is to dwell specifically on the cost saving sources from use of SFA in URC.

Cost Efficiency

At the core of it, the basic premise of such a system, as for most IT investments, is to drive cost savings or to drive revenues more cost effectively. Hence, it’s a given that a successful proposition would come with premise of cost savings. However, how exactly and to what extent specific cost saving opportunities exist in URC is worth listing out, and it is the focus of this blog. While, cost saving can be stretched to include technical aspects like how easy, error free, user friendly, maintainable the system is, since focus of blog is to describe cost savings in URC, I have focused on select heads which are linkedto accruing savings from business use of the system.

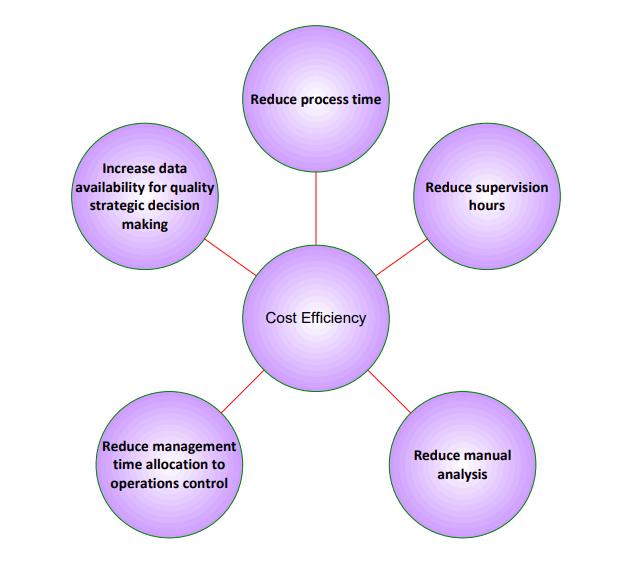

I have listed a few cost savings opportunities that should be possible from adoption of such a solution:

-Reduce process time: The biggest saving opportunity from system is by reducing the process time spend from each sales person, such as order taking, case making, route planning, expense reporting etc. Every hour saved in the process has a magnifying effect as typically a large field workforce is involved hence there is a multiplier effect with large number of processes taking place every day.

- Reduce supervision hours: A key outcome is reduction of supervision hours, with aspects like automated suggested beat plan, deviation reporting, auto fill functions when taking customer inputs via surveys etc, supervision time can be substantially reduced freeing manpower for more strategic aspects. This has a multiplier effect too because it applies at all levels and across the board.

- Reduce manual analysis: Typically, organizations deploy backend systems & manpower to make sense of vast swathes of data flowing through, creation of customized reports via use of specialized tools etc. The system must offer an opportunity to tailor reporting in a manner where it can be directly consumed by decision makers, thereby significantly reducing cost of analysis- licenses, manpower and services. Hence extent of reporting available from system is a factor for cost saving.

- Reduce operations control cost: An effective system must have intelligence built in to recognize exceptional conditions with obvious corrective actions. Hence detection of exceptional conditions, alerting via pre-defined rules and analytics enables proactive decisions, thus on one hand reducing manual detection cost of hours and on the other, stemming cost ‘leakage’ from proactive operations management.

- Increase data availability for quality strategic decision making: Though sounds similar to previous two points, reference here is to ‘completeness’ of information for decision making. The system must be extensible to incorporate major relevant Business Intelligence inputs via correlating and drill down reports that allow for strategic decisions to be made by use of system. To elaborate, if say system delivers information on field sales, but not correlation to competitor promotions running on same system, then it represents lost time, hence cost, for collating data from different systems.

- Operation optimization related savings: There are some areas where cost savings come from optimizations calculated by system- examples are: shorter travel route, expense capturing at point of incurring expenses, auto derived schedule or beat plan etc.

To summarize:

Conclusion

While any automation initiative will likely include cost saving premise, cost savings from using the system in operations in URC should be the key focus for evaluating cost saving potential. In this blog, I have listed a few heads that can be further broken down in specific accounting heads to calculate savings accrual and hence ROI.

See you soon with more…

- Anupam Ahluwalia.